There’s Smoke in the Kitchen Again. And Investors Are Ignoring It.

March 3, 2023, is burned into my memory.

Not because it was interesting. Because it was a warning.

I flew out to Denver a day early to get extra time on the slopes. Land in Denver, grab the truck, and drive up to Keystone through the Continental Divide. Get in a half day on the mountain, hit the Kings, get a fire going, go to sleep.

The first two days were smooth. Snow was perfect. My legs were under me.

Then Sunday hit.

Feeling good after a couple of strong days, I pushed off-trail. Out there, they call it off-piste. The result is the same, no matter what you call it. I may have been showing off when I hit something I didn’t see. My skis went one way, my body went another.

Five minutes later I was finishing the run, knowing I had done damage. A stop at the mountain clinic confirmed it. Two fractured ribs. Trip over.

But that wasn’t the real story. It was just the setup.

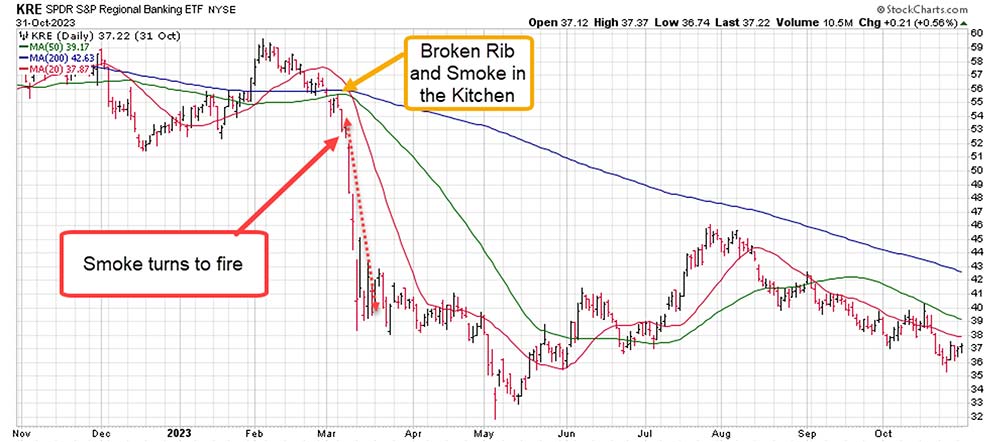

Smoke in the Kitchen

Before I ever set foot on that mountain, I had been watching the regional banks. One name kept showing up in talks, in headlines, in quiet discussions that didn’t make the front page yet. Silicon Valley Bank.

The tone wasn’t panic. It wasn’t calm either. It was the kind of noise that experienced traders learn not to ignore.

That weekend I mapped out scenarios. If Silicon Valley Bank were to fail, what would it mean for the broader financial system? What would it mean for portfolios heavy in financials?

Those questions mattered. Financials don’t operate alone. When they move, they take the rest of the market with them.

On the morning of March 6, at 4 a.m, I was on my way to the airport with broken ribs. The story started to break. Silicon Valley Bank was selling bonds to shore up its balance sheet. TV framed it as a smart move. Responsible. Controlled.

If you have been around long enough, you know what that actually is. It is a liquidity signal. A sign that a bank cannot meet its debts from normal income and is selling assets to raise cash fast.

Sitting in the Delta Club in Denver, ribs wrapped, laptop open, I wrote a note I still remember word-for-word.

“There’s smoke in the kitchen. Look for fire.”

That wasn’t about one bank. It was about a system starting to show stress.

The Rest of the Story

We put protection in place, setting up for downside in financials before things got worse. I got on my plane to Cincinnati expecting the regional banks to drop 5% to 10% before I got home.

The banks moved higher. Investors were whistling past the graveyard.

But then it happened. Within days, the pressure spread. Regional banks sold off hard. Silicon Valley Bank failed. Signature Bank followed.

What started as background noise turned into a full-blown liquidity event. That is a sudden freeze where sellers flood the market, and prices drop fast because no one can get out.

The regional bank ETF dropped roughly 30% in less than a week. The prep paid off. Not just in protection but in a chance to profit.

That matters now because I am getting the same signal again.

Find out what’s going on… and how you can protect yourself…

Cockroaches in the Kitchen

The headline is different this time. The structure is the same. The word that keeps coming up is liquidity. And the source of that concern is private credit.

Private credit is lending that happens outside banks. Think direct loans to companies made by funds, not your local bank. This market has grown to more than $ 1.5 trillion. It was built during years of near-zero rates when debt was cheap, and risk was easy to ignore. That world is gone.

In October 2025, Jamie Dimon, CEO of JPMorgan Chase, pointed to defaults like First Brands and Tricolor as early signs of stress.

He called it a cockroach moment. His point was simple. One default is rarely alone. It signals broader, hidden rot building beneath the surface.

The problem is that much of this exposure sits in funds that are not marked to market. Marked to market means an asset’s value is updated daily to reflect what it would sell for right now. Private credit funds don’t do that.

Their values are updated rarely. The losses building inside them are not visible yet.

On the surface, everything looks stable. Returns look smooth. Yields look good. But that calm is a function of slow pricing, not real health.

Beneath the surface, credit is getting worse. Many of these loans go to highly leveraged firms with weak covenant protection. A covenant is a rule a borrower must follow to stay in good standing with their lender. When covenants are weak, lenders can’t act before a borrower gets into real trouble.

Dumb Things

In February 2026, Dimon reiterated his warning. He said rivals are once again doing dumb things in credit to chase income.

He drew a direct line to the years before 2008. Risk grew late in the cycle under pressure to maintain high returns. Capital is being put to work at the worst point in the cycle. That is the setup that leads to bad pricing and eventual liquidity stress.

The link to 2007 is clear. Back then, the issue wasn’t just bad mortgages. It was the way risk was packed, spread, and mispriced. Exposure moved off balance sheets.

Models hid real risk. The system looked fine until cash dried up. When that happened, it didn’t unwind slowly. It all happened at once.

What This Means for You

The charts in financials are now telling the same story the numbers are.

The Financial Select Sector SPDR ETF has broken below key moving averages. It just completed a Death Cross.

A Death Cross forms when a stock’s 50-day moving average drops below its 200-day moving average. It means near-term momentum has turned negative.

Regional banks look the same. This is happening despite strong earnings last quarter. Prices dropped even as results held up. That tells you the bar is still too high.

Per FactSet, financials posted some of the strongest earnings growth in the market last quarter. The sector is still trading 13% below where it was heading into that season. When the bar stays high in a weak environment, even good results can cause selling.

I don’t think financials can clear that bar in April. Not with the private credit stress behind them.

Retail investors are also more deeply involved in private credit than most realize. High yields in the double digits are the draw. Just like in 2007, investors are trusting models over market prices. That creates a false calm that holds right up until it doesn’t.

We are already seeing more requests to withdraw funds from private credit and private equity funds. Some funds have started to limit those withdrawals.

That only happens when there is a gap between the cash people want out and the assets the fund holds. When that pressure builds, managers have two options. They gate the fund, meaning they restrict how much investors can take out.

Or they sell assets into a weak market. Neither is good.

This kind of stress spreads. Private credit is tied to banks, pensions, and insurance firms. When pressure builds in one area, it moves through the system.

What Would Make Me Wrong

If private credit stress stays contained and doesn’t hit public markets, financials could bounce faster than expected. If earnings beat by a wide margin, the mood could shift. Those are the things to watch. But the weight of the evidence points one way.

The Play

The plan mirrors March 2023.

Both the SPDR Financial ETF and the SPDR Regional Bank ETF have broken down on the charts. Both are below their 50-day moving averages. The SPDR Financial ETF just posted a Death Cross.

Earnings season is the potential trigger. It is coming fast.

For protection, the ProShares UltraShort Financial ETF is back in my playbook. UltraShort means this ETF is built to move twice the inverse of the financial sector. If financials drop 10 percent, this ETF is built to gain roughly 20 percent. Priced at 32 dollars, SKF shares have already gained 26 percent in 2026. I am targeting a move to 40 dollars over the next three months. That is another 25 percent from here.

![]()

YOUR ACTION PLAN

For investors with options approval, the XLF September 18 2026 48-dollar puts are a solid hedge. A put option gives you the right to sell shares at a set price by a set date. It gains value when the ETF falls. Out-of-the-money means the strike price is below the ETF’s current price. That makes it cheaper but requires a bigger move to pay off.

These puts cost 2.65 dollars per contract. My near-term target for XLF is 45 dollars. I see a real shot at 40 dollars through the summer. At 40 dollars, the intrinsic value of the put would be 8 dollars per contract. Intrinsic value is the built-in gain from the gap between the strike price and the current price. Add time premium on top.

Pro Tip: Don’t get greedy. This is a hedge, not a home run swing.

Pro Tip 2: Luck prefers the prepared trader. Start thinking now about how you would reinvest any proceeds from this hedge. That is how you win the long game.

For more insight like this, make sure to check our YouTube channel.