Tesla Tanks 8%, IBM Disappoints – Meanwhile My April Pick Delivered 120% EBITDA Growth

Tesla crashes 8% on earnings. IBM disappoints and drops. S&P hits records.

Same old earnings roulette that separates tourists from professionals.

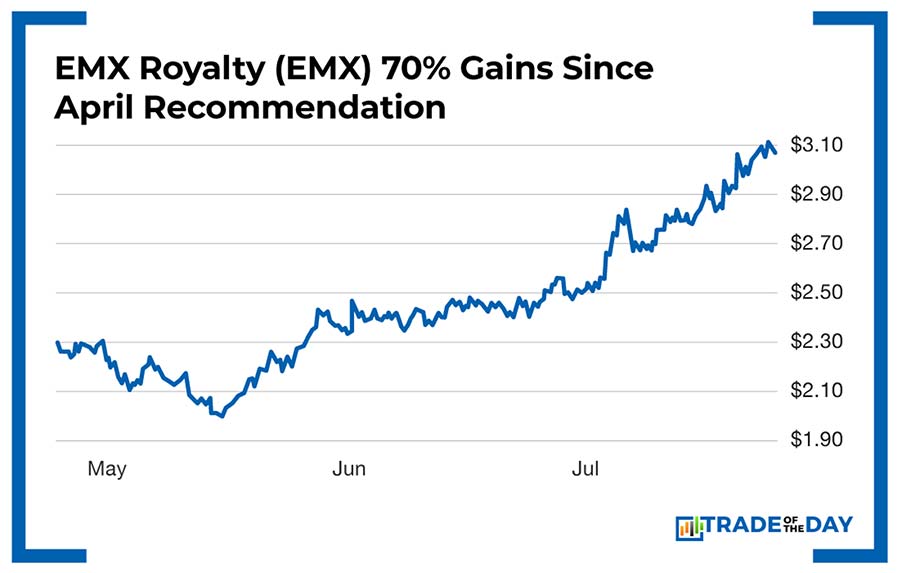

While everyone panicked over quarterly results today, I’m sitting on EMX Royalty – up 70% since my April recommendation – that delivered 120% EBITDA growth back in May while the market was too busy chasing AI stocks to notice.

Here’s what smart money figured out while everyone else was gambling on earnings beats:

The Company That Gets Paid Whether Others Succeed or Fail

Back in May, when EMX reported their Q1 numbers, the market completely ignored them. Too distracted by the latest AI earnings circus to pay attention to a company that had just delivered:

- 40% revenue growth (to $10.8M adjusted royalty revenue)

- 120% EBITDA growth (to $7.1M)

- $36.1M working capital fortress

Why the disconnect? Because EMX doesn’t fit the quarterly earnings narrative Wall Street obsesses over.

They don’t dig holes.

They don’t worry about labor strikes or equipment failures.

They find viable projects, sell them to operators, and collect a percentage of everything that comes out of the ground. Forever.

Think about it: While Tesla’s auto revenue falls for the second straight quarter, EMX deposited another royalty check from mines they sold years ago.

IBM misses software targets? EMX doesn’t care – their “software” is geological surveys that became perpetual income streams.

Gold miners are glorified construction companies. Royalty companies are banks that get paid forever.

The Numbers That Prove Royalty Superiority

Here’s the mathematical reality most people miss:

EMX has 250+ projects across precious metals, base metals, AND battery metals. When Tesla crashes on one bad quarter, EMX collects from:

- Gediktepe copper (Turkey): $4.3M revenue in Q1

- Caserones copper (Chile): $3.0M revenue in Q1

- Timok copper-gold (Serbia): $1.6M revenue in Q1

- Plus 247 other revenue streams

Each discovery becomes another royalty stream. Each metal price increase multiplies their cash flow. Each partner’s success = EMX success, without the operational risk.

The 2026 Catalyst Stack Nobody’s Pricing In

While everyone argues about this quarter’s AI spending ROI, EMX has a pipeline of catalysts that start paying in 2026:

- Chapi Mine: New 2% copper royalty (cost: $7M, starts paying 2026)

- Diablillos: Construction decision H2 2026

- Viscaria Sweden: Final permits approved – construction ready

- Gediktepe expansion: Q1 2026 commissioning

This isn’t speculation. These are specific, dated catalysts with defined timelines.

The Fed-Proof, Recession-Proof Model

Here’s the beautiful part about EMX’s model:

- Gold up = bigger royalty checks

- Gold down = still getting royalty checks

- Fed raises rates = international gold demand increases

- Fed cuts rates = dollar weakens, gold rallies

- Recession hits = metals still get mined, royalties still get paid

While Tesla lives and dies by quarterly consumer demand, EMX gets paid regardless of economic cycles.

![]()

YOUR ACTION PLAN

Most investors buy companies that panic on earnings misses. I buy companies that delivered 120% EBITDA growth while everyone was distracted by the latest shiny object.

At 70% gains, EMX isn’t overvalued – it’s undernoticed. Because in a world where Tesla can crater 8% on one earnings report, wouldn’t you rather own the company that gets paid whether their 250+ partners hit targets or not?

Because while everyone else gambles on quarterly results, we collect checks from other people’s operations.

The house always wins. Be the house.

More from Trade of the Day

How To Buy SpaceX Below Its IPO Price

Jun 19, 2026

The Options Market Is About to Change Forever

Jun 18, 2026

Why I Look Forward to the Slowest Months of the Year

Jun 17, 2026

Everyone’s a Genius at All-Time Highs

Jun 16, 2026