The Real Risk Behind the SpaceX IPO Has Nothing to Do with SpaceX

The SpaceX IPO is just weeks away, with June 12 shaping up to be one of the most anticipated events in stock market history.

If current valuation estimates near $2 trillion are accurate, SpaceX will immediately become the largest IPO ever launched.

And while investors are giddy like toddlers on Christmas, it’s not all sunshine and rainbows…

We may be underestimating just how disruptive this event could become.

Not because of the excitement surrounding the deal, but because of the structural mechanics that would follow immediately afterward.

The media won’t mention it, but this disruption is exactly what you should be keeping an eye on.

There are two separate risks developing here.

The first is psychological or a sentiment risk.

The second is purely mechanical. Something that IS going to happen, not may happen.

Both matter to your portfolio and could change the current trajectory of the market.

SpaceX’s Sentiment Risk

Markets rarely top out when investors are fearful.

They top out when excitement reaches extreme levels and investors believe there’s no reason to worry. That environment has been building for months.

We’ve watched as stocks continued climbing a massive “Wall of Worry” despite geopolitical instability, elevated valuations, slowing economic growth, interest rate uncertainty, and increasingly concentrated leadership.

At the center of that rally has been the AI trade, particularly semiconductors and speculative growth stocks tied to infrastructure spending.

Since April, these stocks have climbed more than 50% as a group. Think about it, that’s two years of average gains in just 40 trading days.

Now combine the enthusiasm behind that rally with the largest IPO in modern market history.

It multiplies the potential “hangover” effect that investors could be facing as stocks party like there’s no tomorrow.

Investors have been waiting for a SpaceX IPO for years.

The anticipation alone has become part of the narrative. Historically, when a single event becomes this emotionally charged, it often coincides with short-term exhaustion rather than the beginning of a new leg higher.

Bryan Botarelli wrote earlier this week about not chasing the SpaceX IPO higher out of the gate.

That doesn’t mean the market will crash immediately afterward.

But it does create conditions where investors finally pause, take profits, and reassess risk.

It’s also possible that investors have already been stockpiling cash specifically to deploy to the IPO itself… If that is true, then June 12 could represent the one final surge of speculative capital entering the market all at once.

Ironically, that may be the exact type of sentiment signal investors should be watching carefully.

What comes next?

If the market struggles to follow through after the IPO excitement fades, the weakness will likely spread into the already stretched semiconductor sector and broader AI trade.

The Bigger Risk May Be Structural

The more impactful issue may be the mechanics that follow SpaceX’s IPO, something that can’t be avoided.

If SpaceX debuts anywhere near the rumored valuation range between $1.5 and $2 trillion, the company would instantly become one of the largest components in the entire Nasdaq-100.

This immediately creates a problem for the index.

It already operates under concentration limits designed to prevent a handful of mega-cap stocks from becoming too dominant.

Remember when this became a major issue in 2023, and the Nasdaq was forced to conduct a special rebalance? It was due to companies like NVIDIA (NVDA), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), and Meta (META) growing too large relative to the rest of the index.

A SpaceX addition could trigger a very similar event almost immediately.

This is why the market is unlikely to see a simple “plug-and-play” addition where one smaller stock gets removed and SpaceX quietly takes its place.

The math just doesn’t work.

Even if Nasdaq removed several of the smallest components in the index entirely, those companies still would not provide enough weighting capacity to absorb a new entrant commanding 4% to 6% of the entire index.

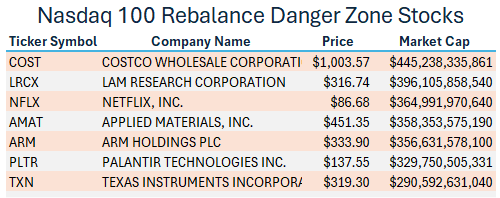

Here are your bottom five stocks – by market cap – in the index. These are at-risk of being dropped because of the special rebalancing.

My money is on Charter Communications (CHTR) getting cut not only because of its small market cap, but also the stock’s -65% performance over the last year.

The Most Likely Outcome

The most realistic scenario is a broader modified rebalance.

In this situation, Nasdaq would add SpaceX while simultaneously reducing the weighting of multiple existing components throughout the index.

That matters because trillions of dollars passively track the Nasdaq-100 through ETFs, retirement portfolios, institutional mandates, and quantitative strategies.

Even relatively small percentage changes can trigger billions of dollars in forced institutional buying and selling.

The point is, SpaceX will not result in normal post-IPO behavior.

Instead, this will behave more like a structural reshuffling of institutional ownership across the entire technology sector.

The important nuance here is that the biggest volatility may not occur in the smallest companies inside the index.

Instead, the pressure zone may shift into the middle-upper tier of the Nasdaq-100.

Why the Middle Tier May Get Hit Hardest

Most investors assume the smallest companies in the index face the greatest risk because they could be removed entirely.

That’s partially true.

But mathematically, those smaller companies barely contribute enough weighting to fund a massive new addition like SpaceX.

A stock carrying a 0.3% or 0.5% weighting simply doesn’t move the needle.

But reducing a company carrying a 2% or 3% weighting creates immediate capacity.

That shifts the likely funding pressure into stocks ranked roughly between eight and 25 in the index. These companies are large enough to matter, liquid enough for institutions to trade aggressively, and heavily owned by passive funds.

This is where investors should focus their attention.

Many of these stocks are already crowded AI-theme trades with heavy institutional ownership and passive ETF exposure, a combination where forced reweighting can temporarily override fundamentals.

Names like Palantir (PLTR) and Arm (ARM) carry elevated speculative positioning, while Applied Materials (AMAT) and Lam Research (LRCX) are tied to semiconductor and AI capital expenditure trends.

Those are precisely the types of names where mechanical selling pressure can create outsized short-term volatility.

Mega-caps will likely shed some weight, but historically the Nasdaq protects its largest companies to preserve market stability. Meaning the “shock absorber” often becomes the tier beneath them.

That’s exactly where most of today’s crowded AI and momentum trades currently sit.

Bottom Line

The SpaceX IPO looks less like a standard IPO and more like a tectonic index event.

That doesn’t automatically mean the bull market ends on June 12…

But when the excitement fades, that combination of euphoric sentiment, crowded trades, and forced institutional selling could send volatility sharply higher.

More from Trade of the Day

Gold Just Went on Sale – But the Reason Won’t Last

Jul 17, 2026

The Market Feels Different. Here’s What To Watch.

Jul 16, 2026

Saddle Up Sally! The Hottest Trend in Retail

Jul 15, 2026